Strong Prices Seen Across Regions For 2013

UK - Prices across Eire, Northern Ireland and the United Kingdom have all been buoyant this year and with tight supplies forecast, such prices are expected to remain, write market analysts at the Livestock and Meat Commission for Northern Ireland. 1 July 2013

1 July 2013

2 minute read

2 minute read

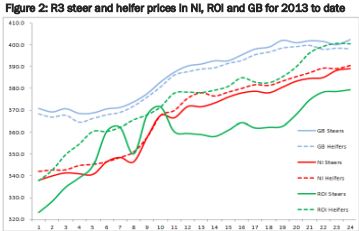

Relatively tight supplies of cattle during2013to date has resulted in an increase in the prices being paid for prime cattle. Figure 2 displays the R3 steer(solid lines) and heifer price (dashed line) in NI,ROI and GB during 2013 to date.

The NI R3 heifer price has increased from 342.1p/kg in the week ending 5 January 2013 to 390.6p/kg in the week ending 22 June 2013. This represents an increase of 48.5p/kg, a 14.2 per cent increase.

The NI R3 heifer price has been consistently behind the ROI price during 2013 to date as indicated in Figure 2. Meanwhile the ROI price was consistently below the GB R3 heifer price until the week ending the 25 May 2013 when strong increases in the ROI R3 heifer price put it above the average GB price for several weeks.

Last week the R3 heifer price in ROI dipped by 1p/kg and was half a penny behind the GB price with an equivalent price of 399.5p/kg. The trade for finished cattle in GB showed a slight improvement last week after several weeks of prices easing slightly as indicated in Figure 2.

The strong increase in the R3 heifer price in ROI since early May has been attributed to a high proportion of heifers being slaughtered fitting into industry specifications. These slaughter specifications vary between processors and by customer but generally include being within specification for weight, age, grade and Bord Bia Farm Quality Assured status.

Reports have indicated that the meeting of these specifications by a large proportion of the heifer kill in ROI allows heifer carcases to be used to fulfil a large proportion of orders and thus the strong demand for heifer beef.

The ability of ROI producers to get heifers to meet industry specifications at point of slaughter more easily than steers has created a significant differential in the prices being paid by the plants in ROI as indicated in Figure 2.

Industry sources have indicated that producers in ROI have had difficulties in getting steers to kill within specification, particularly when considering carcase weight and age at slaughter.

The differential between R3 steers and heifers in ROI last week was 20.8p/kg. Meanwhile in GB and in NI R3 steers and heifers have tended to be closer in price for the year to date as shown in Figure 2.

However if we consider the R3 steer price for 2013 to date for NI, ROI and the GB average there is a slightly different trend. The GB price has gradually increased throughout 2013 and has been consistently above the ROI and NI price with an average price last week of 402.7p/kg.

Meanwhile the prices paid in NI and ROI have also shown gradual increases over the period in question with the NI price consistently above the ROI price since early March.

The R3 steer price in NI last week was 391.1p/kg while it was 378.7p/kg in ROI. With producers busy with other on farm activities the availability of cattle for slaughter is expected to remain fairly tight in the weeks ahead.

This should help underpin current prime cattle prices.

TheCattleSite News Desk