Softening Fed Cattle Price Expectations

US - Much of the conversation in the cattle market over the last several months (years, even) has focused on declining cattle numbers and the supply-side support for prices that will characterize the market for the foreseeable future, writes John D. Anderson, Deputy Chief Economist at the American Farm Bureau Federation. 18 February 2013

18 February 2013

3 minute read

3 minute read

The recent inventory report (discussed by Dr. Tonsor in last week’s ICM newsletter) provided confirmation of this decline in numbers. In the context of this fresh information on contracting cattle supplies, the behavior of cattle futures prices is worth noting.

In mid-December last year, the April Live Cattle contract on the CME traded as high as $138. The December contract got within about 50 cents of that level as well.

These price expectations were largely based on expectations of tight meat supplies and continued slow but steady economic growth. However, since that mid-December peak, Live Cattle futures prices have dropped substantially.

This week, the April contract has traded (briefly) below $128; and the December contract has traded down to around $130. This decline in Live Cattle prices has, of course, been accompanied by a decline in Feeder Cattle futures prices as well.

So, why the deterioration in price expectations? The Cattle report just confirmed tighter numbers. Notwithstanding a dip in real GDP in the fourth quarter last year, other economic indicators are not really out of line with where they have been for many months and some (home prices, for example) have shown notable improvement – which should be firming up the demand side of expectations.

One thing that has changed considerably since late last year is expectations of total meat production in 2013. While smaller cattle inventories point to smaller beef production down the road, short-run expectations for beef production have been revised steadily higher since about last November.

For example, last week’s World Agricultural Supply and Demand Estimates (WASDE) report from USDA included a forecast for first quarter beef production of just over 6.3 billion pounds. That’s nearly 4 percent higher than their 2013.Q1 forecast from last November (which was a bit less than 6.1 billion pounds).

Production estimates for quarters two through four have also been revised up by 1.5 to 2 per cent. Not surprisingly, the report cites heavier carcass weights as accounting for much of the adjustment, with the larger first quarter adjustment also reflecting higher cow slaughter.

Perhaps more significantly, the WASDE report also shows changing expectations regarding competing meat supplies. While first-quarter hog production estimates are now slightly lower (less than one-half of one percent) than they were last November, estimates for quarters two through four have been raised by 2 to 4 per cent – with the biggest change applying to fourth quarter forecasts. Broiler production forecasts have also been ratcheted up.

The forecast for second quarter broiler production in last week’s WASDE was over 350 million pounds larger than the forecast in the December WASDE – an increase of about 4 per cent. The third quarter broiler production forecast is up almost 3 per cent from the December figure.

These evolving market expectations highlight a real challenge for the beef industry. While beef production forecasts have been bumped up in recent months, production will still be down substantially from 2012 levels.

It will almost certainly decline further in 2014 as herd rebuilding removes females from the market. Meanwhile, pork and broiler production are back to modest expansion, capitalizing on historically high meat prices and what everyone hopes will be moderating feed prices as this year’s grain crop progresses. These guys are very tough competition – competition that can put a real limit on beef’s upside price potential in a steady (or weak) demand environment.

The Markets

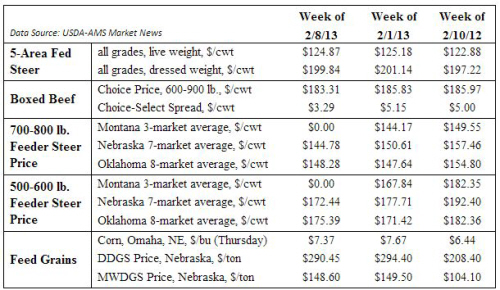

Fed cattle prices were steady to $1 lower across the major feeding regions last week. The 5-area weighted average worked out to post a decline of less than 50 cents for the week.

Negotiated sales were on the light side as steady-to-lower bids generated little enthusiasm in the market.

Calf markets were mixed, with heavier calves called steady to $3 lower. Lighter calves with turn-out potential were firm to $5 higher, with the strongest gains in the Southeast, where spring – and hopefully the grass that comes with it – is just around the corner.

Wholesale beef prices were weaker last week. For the week, the choice cutout averaged around $2.50 less than the prior week, so anyone hoping for a boost from the Plainview plant idling had to be disappointed.

TheCattleSite News Desk