The Middle East conflict: Implications for feed and animal producers

The conflict in the Middle East will cause significant impacts to trade within the agriculture industry, particularly with feed markets and overall supply chain

12 March 2026

12 March 2026

11 minute read

11 minute read

By:

By: The Middle East conflict has triggered one of the most significant and concurrent disruptions to agricultural trade, energy supply, and global logistics in recent history. For feed additive companies, the compounding effects of the Red Sea/Bab el-Mandeb closure, the newly disrupted Strait of Hormuz, rising oil prices, supply chain rerouting, and shifting demand patterns in the world’s fastest-growing feed markets constitute both immediate operational risk and medium-term strategic opportunity.

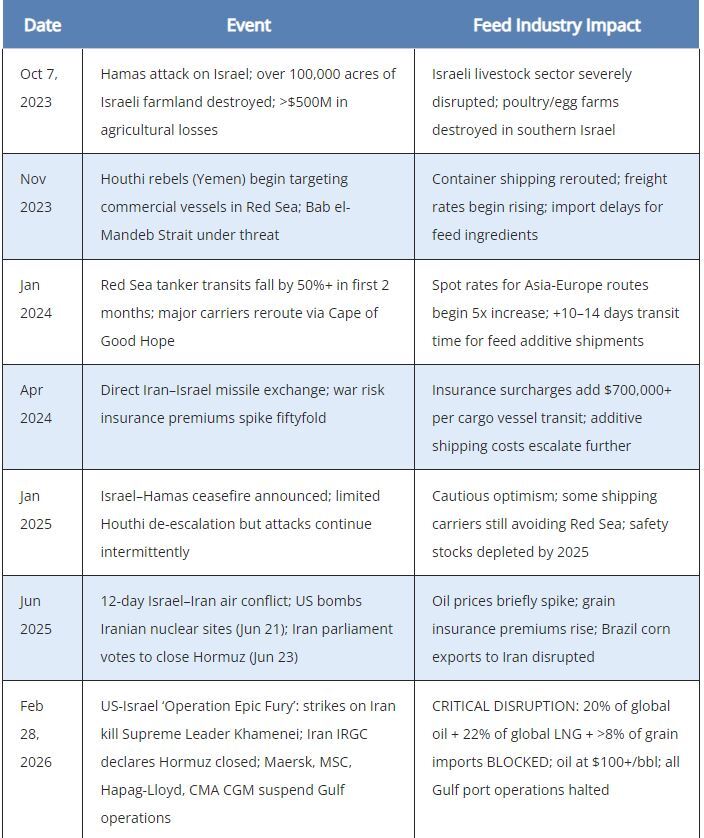

As of February 28, 2026, the US–Israel joint military strikes on Iran have triggered an effective shutdown of the Strait of Hormuz. Maersk, MSC, Hapag-Lloyd, and CMA CGM have all suspended Gulf operations. This is now a TIER-1 supply chain emergency for the feed additive industry.

The current crisis is the product of nearly 30 months of sequential escalation. Understanding the timeline is essential for assessing the cumulative impact on the feed and animal nutrition industry.

Maritime chokepoints: critical bottleneck for the feed industry

The Bab el-Mandeb Strait – the southern entry to the Red Sea – connects the Gulf of Aden to the Indian Ocean. Prior to the conflict, it was the primary artery for Asia–Europe trade, facilitating approximately 15% of global maritime trade and nearly 30% of global container traffic. The humanitarian corridor also carried massive volumes of feed grains, feed additives, vitamins, amino acids, and raw materials from Asian manufacturers (predominantly Chinese) to European and Middle Eastern markets.

The Strait of Hormuz (February 28, 2026 – ACTIVE CRISIS)

STATUS AS OF MARCH 3, 2026: The Strait of Hormuz is experiencing an effective shutdown following US–Israel strikes on Iran on Feb 28, 2026. Iran’s IRGC issued VHF warnings to all vessels. Maersk, MSC, Hapag-Lloyd, and CMA CGM have suspended Gulf operations. This is the most severe maritime disruption in modern history.

The Strait of Hormuz is a 21-mile-wide waterway between Oman and Iran, with effective shipping lanes just 2 miles wide in each direction. It is the world’s most critical energy chokepoint and a vital import corridor for agricultural commodities into the Middle East Gulf (MEG).

Key Hormuz Alternative Routes: Pipeline alternatives exist but cover only ~17% of typical flow volumes:

East–West Pipeline (Saudi Arabia): Capacity ~5M bbl/day; cannot replace 20M bbl/day Hormuz flow

Habshan–Fujairah Pipeline (UAE): Capacity ~1.5M bbl/day; limited impact on total disruption

For agricultural commodities: NO meaningful pipeline alternative exists; full rerouting via Cape of Good Hope is the only option

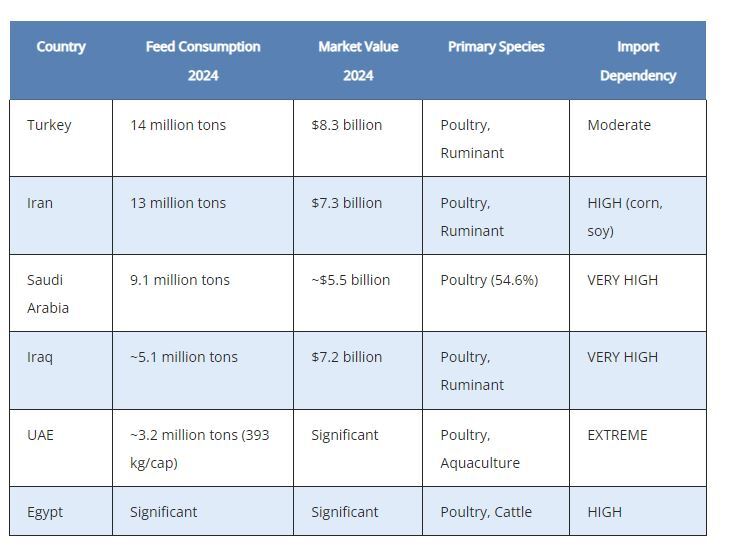

Impact on animal production in the Middle East

Regional Feed Market Context

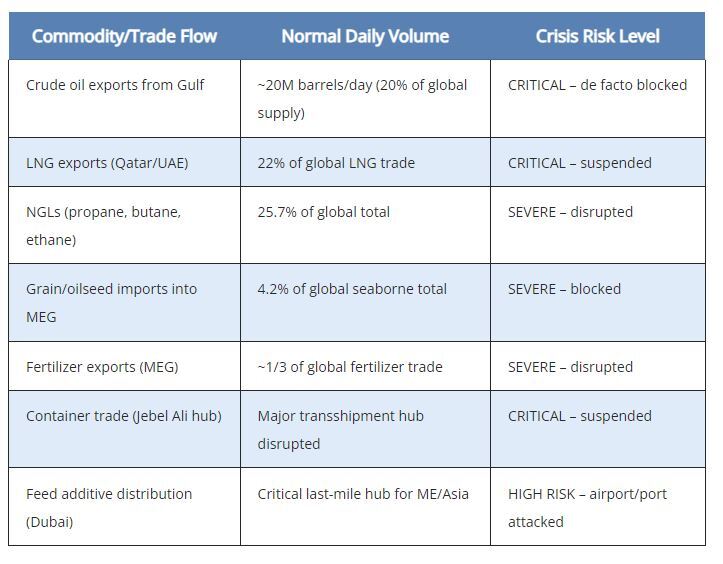

The Middle East and Africa account for approximately 5.9% of world compound feed production, with ~75 million tons/year. The Middle East animal and pet feed market alone was valued at $53.2 billion in 2024, consuming 63 million tons. The region is a net feed importer, heavily dependent on seaborne commodities – a structural vulnerability now severely exposed.

Grain and feed import vulnerability

The Middle East is the world’s largest importer of wheat and rice, and the second largest importer of corn. The Gulf Cooperation Council (GCC) countries are rated as food-secure by conventional metrics – but this masks extreme import dependency. The simultaneous closure of both the Bab el-Mandeb/Red Sea route and the Strait of Hormuz creates a near-complete sea access denial scenario for MEG grain imports.

The MEG accounts for ~4.2% of global seaborne agricultural bulk imports (corn, wheat, barley, soybeans) – about half sourced from Brazil and Argentina (Kpler, Jun 2025)

Iran imports ~4.3 million MT of corn annually from Brazil; in 2025 Iran was Brazil’s #1 corn destination at 24% of total exports (S&P Global, Jun 2025)

Iran’s seaborne agricultural imports fell 38% in 2024 from 2022 highs; the 2026 conflict will accelerate this decline sharply

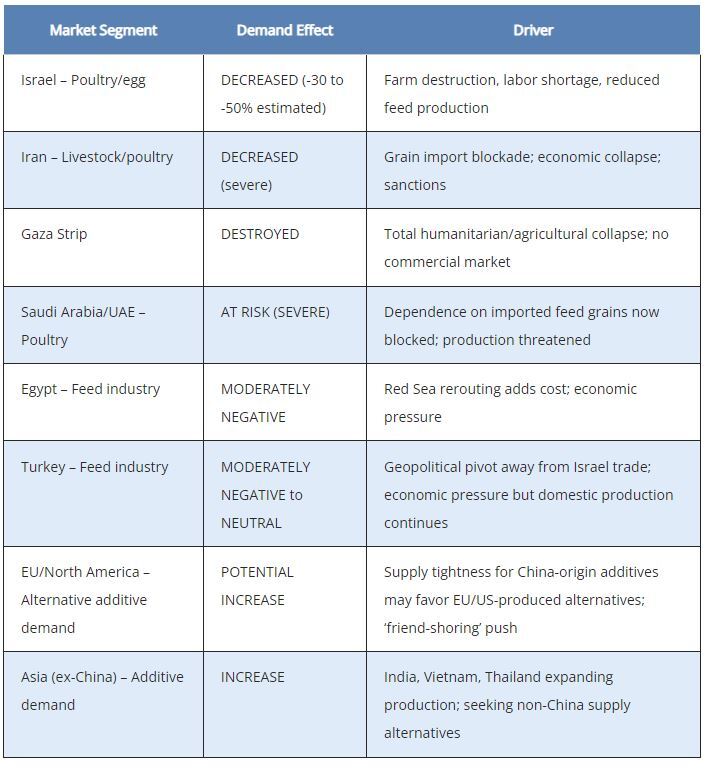

Israel, entirely dependent on corn imports for feed and starch, saw poultry/egg farm destruction in the north and south; wheat stocks remain low (USDA GAIN, 2025)

Australia–Israel cattle shipments disrupted by Red Sea closure (USDA Israel Grain and Feed Annual, 2025)

A December 2024 UN report found 66.1 million people (~14% of the Arab region) faced hunger in 2023; projections for 2026 are materially worse

The simultaneous closure of both the Red Sea/Bab el-Mandeb and the Strait of Hormuz represents an unprecedented ‘double sea blockade’ scenario for Middle Eastern grain and feed importers. Gulf nations with food reserves of 3–6 months face acute shortages if the crisis extends beyond Q2 2026.

Specific country-level animal production impacts

Israel

October 7 attacks destroyed >100,000 acres of farmland and caused >$500M in agricultural income losses (The Media Line, Oct 2024)

Poultry and egg production farms in northern and southern Israel destroyed by Hamas/Hezbollah actions; significant production decline

Labor crisis: up to 1/3 of Thai agricultural workers left immediately; Palestinian workers banned; volunteer-reliant harvest is not sustainable

Israel is entirely dependent on corn imports; barley feed use is reduced due to farm losses

Turkey – formerly among Israel’s top 5 exporters – imposed a full trade ban in 2024; chemical imports from Turkey collapsed from $16M/month to $2M/month

Iran

Iran’s corn imports from Brazil disrupted by rising insurance premiums, payment freezes, and wartime risks even before Feb 2026 escalation

With Hormuz effectively closed, Iran faces catastrophic domestic food supply disruption despite being a net energy exporter

Iranian livestock sector faces acute corn and soybean meal shortages; poultry and ruminant production under severe stress

Gulf States (Saudi Arabia, UAE, Kuwait, Qatar)

GCC countries are rated ‘high’ in food security indices – but are NOT immune to port blockades (World Economic Forum, 2025)

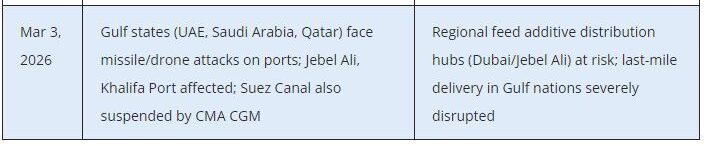

Jebel Ali (UAE) and Khalifa Port are major transshipment hubs for feed and additives serving broader ME/Asia markets – both now affected by missile/drone strikes

Saudi Arabia’s large-scale integrated poultry sector (top 7 producers control 87% of slaughter volume) relies entirely on imported corn, soy, and feed additives

Saudi Arabia’s Balady Poultry expansion plans (200M additional chicks/year) face acute disruption

Feed additive supply chain: Raw material availability and cost impact

Global feed additive market context

The global feed additives market was valued at $37.93–$57.82 billion in 2024 (multiple sources), projected to grow at 4.3–6.3% CAGR to 2032. The Middle East feed additives market reached $0.91 billion in 2025, forecast to grow at 3.2% CAGR to $1.07 billion by 2030. Amino acids dominate with 20.6% share; poultry accounts for 55.7% of volume – both sectors among the hardest hit.

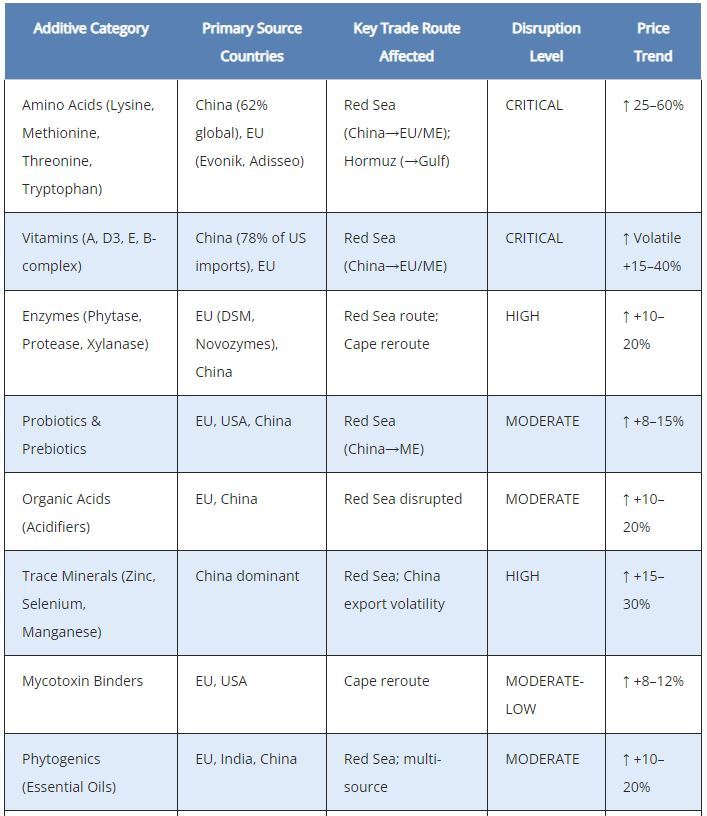

Supply chain dependency map: Key additive categories

The China dependency problem – amplified by the conflict

The Middle East conflict has dramatically amplified pre-existing structural vulnerabilities in feed additive supply chains – above all the heavy dependence on Chinese manufacturing.

The US relied on China for 78% of total vitamin imports and 62% of global amino acid production over 2020–2024 (IFEEDER, November 2025)

US poultry and livestock production uses >425,000 tonnes/year of the top four amino acids and ~50,000 tonnes of supplemental vitamins (AFIA)

Asia-Pacific (dominated by China) accounted for $14.46 billion of the global feed additives market in 2024

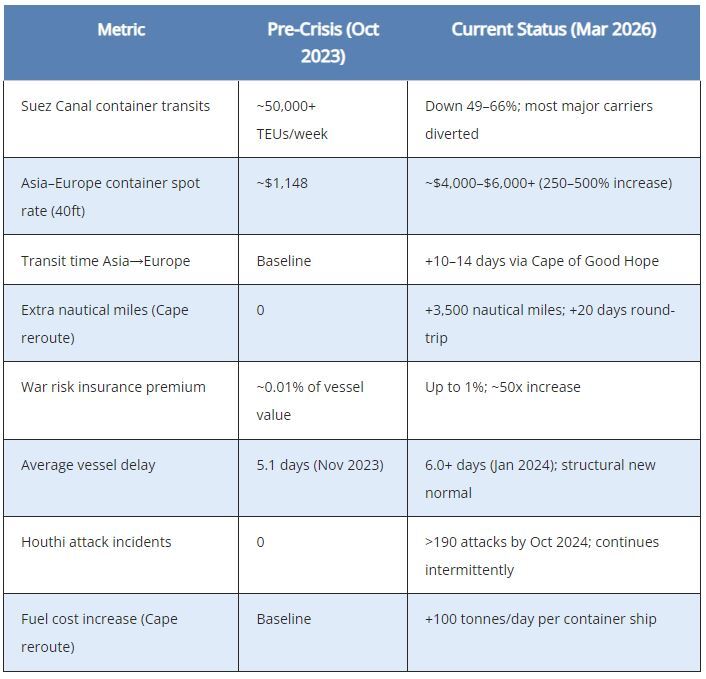

The Red Sea closure adds 10–14 transit days and up to $2,100/container in surcharges on shipments from Chinese ports to European or Middle Eastern destinations

A 40-foot container from China to Europe now costs ~$4,000–$6,000 vs. $1,148 pre-crisis – a 250–500% increase

US tariffs on Chinese feed additives of 25% (imposed 2024–2025) compound the logistics cost surge

Global capacity utilization for vitamins and amino acids has fallen below 80% – the threshold for financial stress on manufacturing viability, driving further price instability (IFEEDER, 2025)

At least 25% of studied vitamins and amino acids had production capacity that was underutilized or idle – including some categories at 20–30% utilization

STRATEGIC RISK: A single geopolitical shock to Chinese production capacity – coinciding with Middle East maritime disruption – would create a catastrophic supply gap for the global animal nutrition industry. The IFEEDER report warns: ‘even a small decline in supply of these important ingredients can have a huge impact on animal health and productivity.’

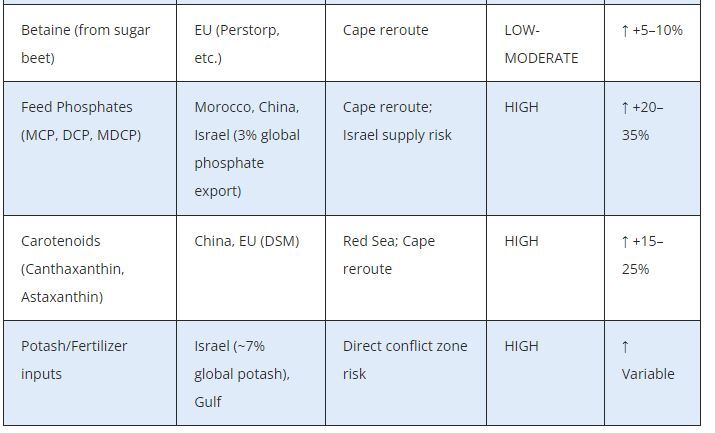

Israel’s phosphate and potash: A secondary supply risk

Israel accounts for ~7% of global potash exports and ~3% of phosphate exports (Rabobank, 2023)

ICL (Israel Chemicals Ltd.), headquartered in Israel, is a major global supplier of phosphate and specialty fertilizers critical for feed-grade minerals

The primary potash/phosphate resources are in the Negev Desert, ~60 miles from Gaza – currently functioning, but with logistics risk

Turkey’s trade ban on Israel has disrupted chemical/mineral supply chains; imports of mineral products from Turkey to Israel fell from $13M to <$1M/month (US Trade.gov, 2024)

In a broader escalation scenario, ICL’s export capabilities could be disrupted, removing a significant share of global phosphate supply

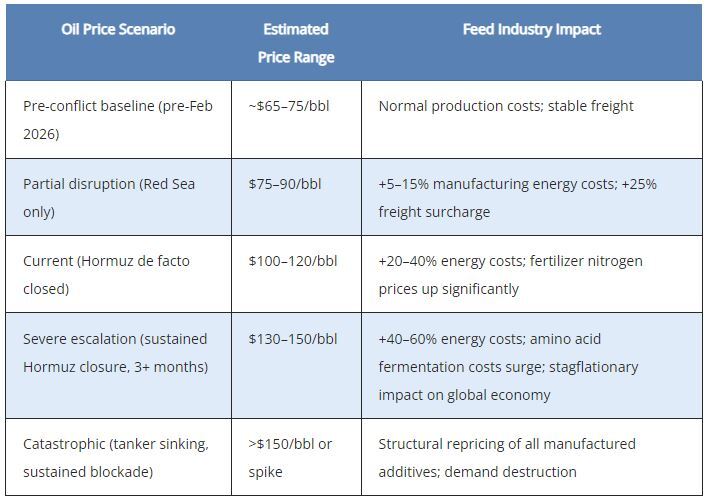

Energy costs: The multiplier effect on feed additive production

Oil prices are the most important cross-cutting variable for the feed additive industry. Nearly all manufacturing inputs – fermentation energy, synthesis energy, transport – are sensitive to oil/gas prices. The Strait of Hormuz crisis has created a direct energy cost shock:

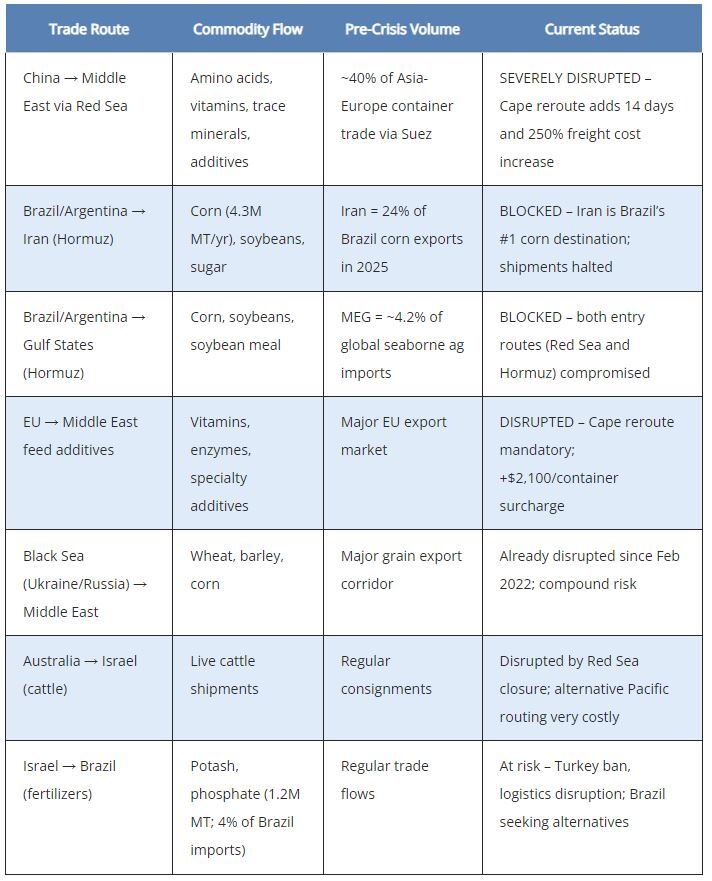

Trade flow changes: Imports, exports and alternative routes

Major trade flow disruptions for feed and feed additives

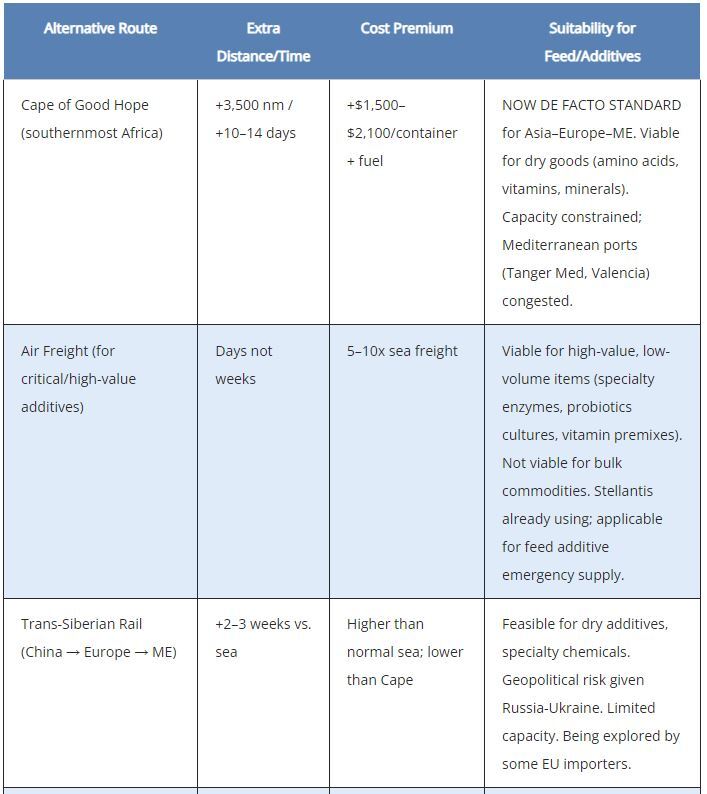

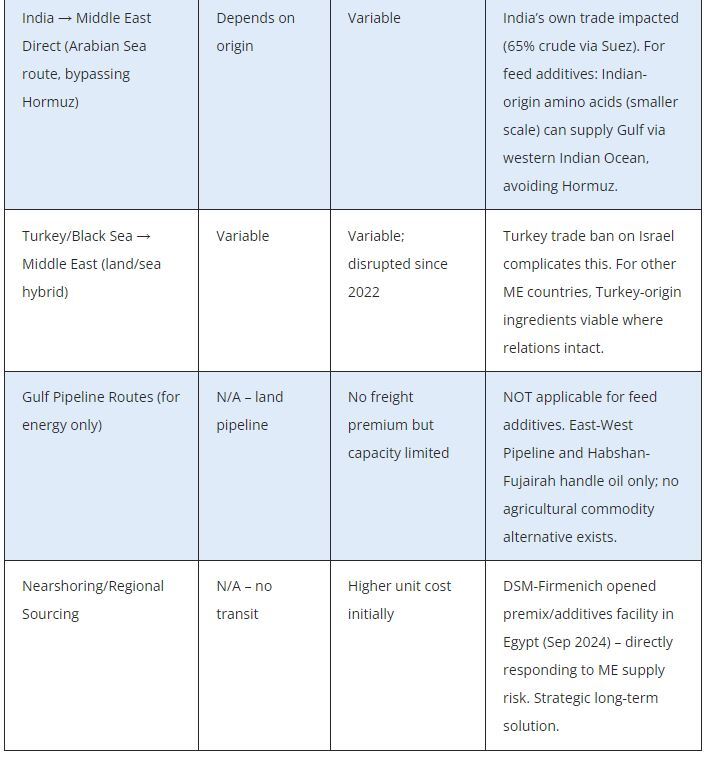

Alternative routes currently being used or considered

Port congestion: Downstream bottlenecks

The rerouting of vessels via the Cape of Good Hope has created significant congestion at western Mediterranean and Atlantic hub ports:

Barcelona experienced a 23.9% increase in container traffic due to Red Sea rerouting

Tanger Med (Morocco) handled an additional 9 million TEUs as a result of Cape rerouting

Jebel Ali (UAE) – the largest port in the Middle East and critical for regional feed additive distribution – is now under direct threat from Iranian missile/drone strikes (Mar 2026)

Port of Fujairah, a key bunker fuel and transshipment hub, has been referenced in UKMTO incident reports (Mar 2026)

Egyptian Suez Canal revenues have fallen dramatically; compounding Egypt’s economic fragility and potential for further regional instability

Strategic implications

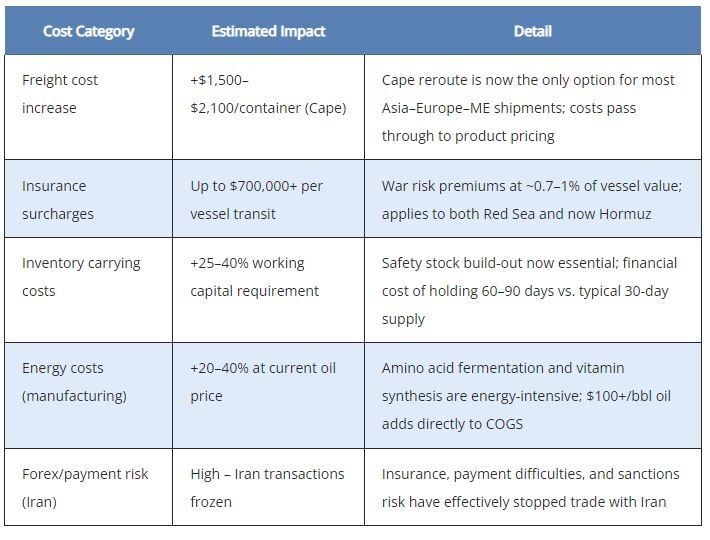

Financial impact analysis

Demand-side effects: Reduced vs. increased additive demand

Regulatory and geopolitical trade complications

Turkey’s blanket import/export ban on Israel has created a significant precedent; further countries may impose quiet embargoes as the Iran conflict widens

US tariffs of 25% on Chinese feed additive imports (effective 2024–2025) add a regulatory layer on top of the logistics cost surge

EU regulatory push toward antibiotic-free production is increasing demand for acidifiers, probiotics, and phytogenics – growth segments still viable but supply-constrained

The IFIF (2024) found that strategic diversification of ingredient sourcing can reduce supply disruption risks by up to 40% – a clear strategic imperative now

The AFIA-supported ‘Securing American Agriculture Act’ specifically targets vitamin/amino acid dependency on China; similar EU initiatives are underway

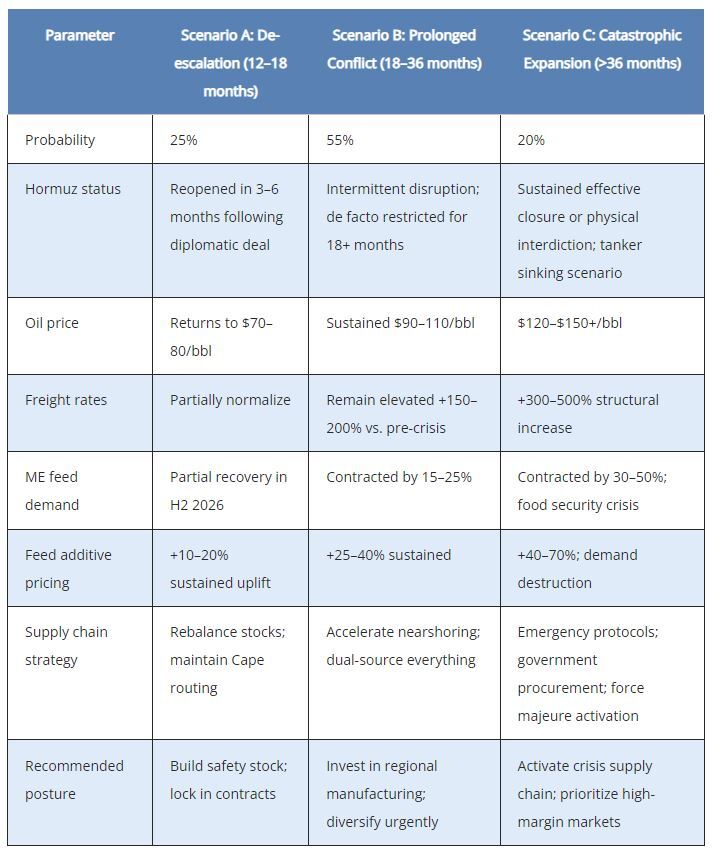

Scenarios and forward outlook (2026-2027)

Based on the current military situation as of March 3, 2026, and historical precedents for similar maritime crises, three scenarios are modeled:

Note: As of March 3, 2026, Scenario B is the most likely base case. The ongoing ceasefire status of the Hormuz crisis remains uncertain; Iran has not formally closed the strait but effective vessel transit has halted.

Strategic recommendations for industry stakeholders:

Immediate actions (0–90 Days)

DECLARE SUPPLY CHAIN EMERGENCY STATUS: Convene crisis team; identify all Gulf-region inventory positions; audit vendor exposure to Hormuz-dependent routes

INVENTORY BUILD: Target 90–120-day safety stock for critical amino acids (methionine, lysine, threonine) and vitamins (A, D3, E, B-complex) sourced from Chinese manufacturers – previously 30 days was standard; safety buffers have been exhausted (Hillebrand Gori, Dec 2025)

CONTRACT LOCK-IN: Negotiate long-term (12–18 month) supply contracts with European-based manufacturers to reduce China routing dependency

ACTIVATE ALTERNATIVE SOURCING: Identify Indian, Korean, or other Asian manufacturers for amino acid intermediates; note that Indian capacity is smaller but available without Hormuz dependency

CUSTOMER COMMUNICATION: Proactively notify Gulf and ME customers of supply risk

REVIEW ALL IRAN POSITIONS: Freeze new commercial exposure; review accounts receivable; engage legal counsel on force majeure clauses in active contracts

Medium-term actions (3–12 Months)

NEARSHORING/REGIONAL MANUFACTURING: Evaluate establishing or partnering for a blending/premix facility in Morocco, Egypt, or Turkey to serve ME/African markets without Hormuz or Red Sea dependency

SUPPLY DIVERSIFICATION: Per IFIF (2024), strategic diversification of ingredient sourcing can reduce supply disruption risk by up to 40% – set a hard target of reducing single-country sourcing above 50% for any critical raw material

DUAL-ROUTING STRATEGY: Qualify Cape of Good Hope as permanent primary routing for all China-origin materials; do not assume Red Sea route will normalize immediately

FREIGHT HEDGING: Explore container freight rate hedging instruments; build surcharge recovery clauses into all forward customer contracts

REFORMULATION SUPPORT: Offer technical service to customers facing feed cost inflation – precision amino acid formulation, reducing excess protein use, enzyme programs to unlock nutrition from lower-cost local ingredients

DIGITAL SUPPLY CHAIN INVESTMENT: Invest in real-time supply chain visibility tools (ETA monitoring, alternative route optimization, insurance cost tracking)

Long-term strategic positioning (12–36 Months)

FRIEND-SHORING: Align sourcing with geopolitically stable allies; prioritize EU, Brazil, India as long-term supply partners – less exposed to specific risks

FOOD SECURITY POSITIONING: Middle Eastern governments (Saudi Arabia 2030 Vision, UAE, Qatar) are heavily investing in domestic food security – position your company as a strategic partner for this transition, not merely a supplier

PRODUCT PORTFOLIO EVOLUTION: The crisis accelerates demand for precision nutrition (lower inclusion rates, higher efficacy), sustainability credentials (reduced environmental footprint), and antibiotic alternatives – invest R&D accordingly

TURKEY OPPORTUNITY: Turkey remains the largest ME feed market (14M tons/year); its geopolitical independence from the ME conflict and improving relations with Gulf states make it a strategic distribution hub