Economic Impacts of Regulatory Responses to BSE

Using Bovine Spongiform Encephalopathy (BSE) as an example, this paper by the United States Department of Agriculture Economic Research Service demonstrates the pervasiveness of the effects of restrictive feed policies and regulations, particularly as they relate to meat and bone meal and other protein feeds. 10 November 2008

10 November 2008

19 minute read

19 minute read

Abstract

Costs evaluated include those assumed by consumers via changes in supplies of secondary and final products; environmental costs associated with disposal of hazardous materials; lost value of products to the rendering industry, including a decline in value of meat and bone meal; and costs of supply disruptions and substitutions within the feed market sector. Benefits from new or amended policies accrue but are not easily measured.

Policy Responses Extend Disease Impacts

The economic effects from animal disease outbreaks include outcomes resulting from policies and regulations designed to mitigate or prevent future disease outbreaks. While the primary motivation for policy responses is to benefit society at large, these policies and regulations can carry significant costs for some sectors that are often pervasive and difficult to identify or quantify, and may have unintended consequences. The distribution of the economic burden of regulations among producers, processors, and consumers varies depending on the producers’ and processors’ ability to pass on the increased costs and consumers’ willingness to pay higher prices for meat. These policy-induced effects can be much greater and much longer lasting than the immediate economic effects of the disease.

Prevention/mitigation policies and regulatory changes related to Bovine Spongiform Encephalopathy (BSE), or mad cow disease, affect a large number and variety of upstream and downstream sectors. Significant among these policies and regulations are those that restrict feeds or feeding, either directly or indirectly, as a means of preventing or mitigating the spread of animal diseases. Using policy and regulatory responses to BSE as an example, this paper demonstrates the range of costs and effects associated with animal disease-related policies and regulations. Costs are easier to estimate than benefits.

The effects from BSE-related feed-policy responses are widespread and extend far beyond the cattle and beef industries. This is due to the number of industries dependent on outputs from the byproduct and rendering industries and feed manufacturing sectors. Affected industries include the cosmetic and pharmaceutical industries (both of which use byproducts, such as gelatin and collagen), feed manufacturing industries, and numerous service and manufacturing industries (which use other animal byproducts, such as enzymes, triglycerides, and other compounds in the manufacture of fatty acids, paints, varnishes, rubber goods, plastics, and lubricants).

Restrictive policies reduce the possible uses of the numerous byproducts and rendered products by cosmetic, pharmaceutical, manufacturing, and other industries. To recoup the lost value, industries must discover new uses for these materials. New regulations can also saddle industries with costs associated with disposal of these hazardous materials in an environmentally benign manner (Informa Economics, 2005; Coffey et al., 2005). In addition, downstream markets for substitutes for the restricted products may be affected, and consumers may be affected via changes in supplies of secondary and final products.

The costs of regulations of byproducts accrue to cosmetic, pharmaceutical, manufacturing, and other industries and their upstream suppliers of intermediate byproducts and offal. For example, costs associated with BSE-related restructuring in upstream (livestock producers, meatpackers, etc.) and downstream (manufacturers of pharmaceuticals, cosmetics, plastics, lubricants, leather goods, etc.) industries are significant. Implications of these costs can vary based on whether the numbers of affected animals are limited (as in the case of BSE) or widespread (as in the case of an outbreak of foot-and-mouth disease). Benefits from animal disease mitigation and prevention policies and regulations, in addition to being difficult to measure, are often spread over a much broader group of beneficiaries, pointing to the need for a broader view of those negatively and positively affected (see, for example, Paarlberg, Lee, and Seitzinger, 2003). BSE-related policies aimed at preventing the spread of the disease among cattle and its human form, variant Creutzfeldt-Jakob disease (vCJD), to humans have had economic effects on grain and protein feed markets since BSE was first discovered in the United Kingdom (UK) in 1986. This analysis focuses on the potential economic effects that can arise from preventive or mitigative policies restricting or altering the use of animal-based feed ingredients, particularly meat and bone meal (MBM) and other proteins.

BSE-Related Feed Regulations

In the case of BSE, in which outbreaks tend to involve relatively small numbers of livestock, policy and regulatory implementation can still result in large changes in protein feedstuff markets. The changes occur even in countries with no confirmed cases of BSE because virtually every country imposes regulations to prevent the spread of the disease (USHHS, FDA, 1997a and b). Further, in concluding their updated risk assessment of BSE in the United States, Cohen and Gray (2005, p. 35-36)) suggest that “[it] is worth noting that [the risk management measures adopted by the U.S. Department of Agriculture, considered by FDA, or proposed by the International Review Subcommittee] reduce what is already a small exposure [to BSE] in absolute terms.” Changes occur in markets for substitutes (e.g., other proteins) and complements (e.g., other feedstuffs fed in conjunction with proteins). Changes in BSE-related feeding policies and regulations also require re-evaluation of the disposal of livestock wastes, as new or expanded uses or means of disposal have to be developed for newly prohibited materials.

A direct impact of implementing preventive and mitigative policies or amended regulations related to animal disease outbreaks can be euthanization of large numbers of livestock. In the short term, a drop in numbers of livestock reduces demand for feeds (grains, proteins, and byproducts) and feeding services (feedlots and other feeding facilities). Disease prevention and mitigation policies and regulations also have a number of indirect effects on feed markets. Restrictions on MBM, for example, can affect prices of other protein feeds.

A Short History of Meat and Bone Meal and BSE

To understand the complex nature of policy-induced effects on feed markets, one should first recognize that animal-based proteins, including MBM and blood meal, are high-quality protein sources rendered from many terrestrial and aquatic animals that are important feeds for livestock worldwide. Prior to 1997, no distinction was made between MBM derived from ruminants (animals whose stomachs have multiple compartments) and that from nonruminants (animals whose stomachs have a single compartment), and MBM represented an additional source of both protein for animal feeds and revenue for renderers and packers. MBM’s contribution to total protein supplies had the effect of reducing costs of animal feeds. MBM’s contribution to packers/renderers increased the value of livestock, ultimately increasing cattle prices, while lowering the prices consumers paid for meat. In the United States, as recently as 2000, most MBM was fed to poultry (45 percent), pets (25 percent), swine (15 percent), and cattle (10 percent, nonruminant MBM) (Coffey et al., 2005).

MBM and other animal-derived proteins continue to be important sources of protein for nonruminants in the United States. Vegetable proteins (soybean meal, cottonseed meal, and distillers’ byproducts), nonprotein nitrogen (urea), and, increasingly, distillers’ grains are often more commonly fed to ruminants because they are generally cheaper sources of protein. These types of feed are especially suitable for ruminants because they can convert vegetable proteins and urea to high-quality protein in the rumen (one compartment of the stomach).

In the United States, most protein in cattle rations is fed to lactating dairy cows and cattle being fattened in feedlots during the final few months prior to slaughter. Dairy cows and calves account for most of the 70 percent of blood meal used by ruminants (Sparks, 2001). Even before FDA prohibited feeding protein derived from ruminants, other than blood products, to ruminants in August 1997, only small amounts of animal proteins were fed to ruminants in the United States, primarily to dairy cattle, because of the relatively high cost of this type of feed. Range cattle, which are on pasture most of their lives, typically receive little protein supplement of any kind.

In the European Union (EU), inadequate production of protein feeds and tariff structures on grains were such that animal proteins were priced more competitively with vegetable proteins (Hasha, 2002). EU producers made wide use of MBM in cattle feed rations before the EU feed ban. This practice, along with changes in the rendering process in the EU, is thought to have contributed to the spread of BSE, particularly in the UK. In an ex ante analysis, it was estimated that the 2001 EU ban against MBM in any animal feed would cause the EU to import an additional 1.5 million more tons of soymeal per year to replace meat and bone meal in livestock feed rations (USDA, OCE, 2002).

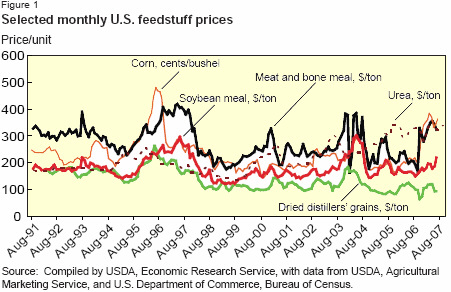

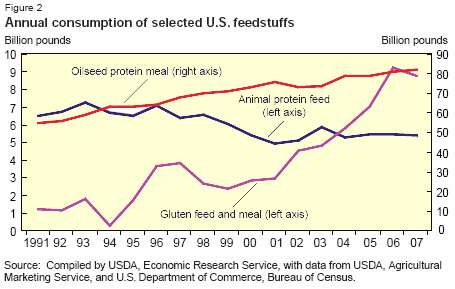

Even before the discovery of BSE in North America, some U.S. poultry producers had reduced their use of MBM in poultry feed rations, in part, as a response to BSE-related problems in the EU. U.S. producers were also likely heavily influenced by the 1996 UK announcement of a possible connection between BSE and vCJD in humans. As MBM use in the United States declined, prices for substitute sources of high-quality livestock protein feedstuffs increased, although prices for proteins continued to move together, despite regulatory effects on MBM (figs. 1, 2).

Benchmark BSE Events

Four periods have been marked by benchmark BSE events that resulted in regulatory/policy responses (Mathews et al., 2003; Mathews et al., 2006). In 1986, cattle were found to be infected with a new Transmissible Spongiform Encephalopathy (TSE), a group of neurological diseases affecting several mammalian species. First discovered in the UK, the disease—BSE—was considered by most countries to be an animal health issue, and various restrictions, including those on trade, were imposed on the basis of protecting animal health.

In 1996, BSE-related regulations shifted significantly with the discovery of BSE-infected cattle in EU countries other than the UK (France, Ireland, and Portugal) and, more importantly, with the announcement in March 1996 of a potential link between vCJD in humans and BSE in cattle. In 2000, native-born BSE cases were discovered in other EU countries and in countries outside the EU (e.g., Japan in 2001). Lastly, in 2003, BSE was discovered in a cow in Canada (May) and in a cow in the United States that had been imported from Canada (December).

The sharp MBM price decline in 1997 in the United States (see fig. 1) was due to the 1997 feed ban, which followed the 1996 UK announcement of a BSE connection with vCJD in humans. Effects of the spread of BSE to other countries are reflected in the increased rate of decline in U.S. MBM production in 2000. The 2003-04 round of BSE-related feed regulations resulted in another sharp decline in U.S. MBM prices in 2004 and 2005.

In the United States, BSE-related feed policies began with an emergency ban on importation of all ruminants and MBM from the UK in 1989 (Coffey et al., 2005). An extension of the ban followed on December 6, 1991, restricting all high-risk products from countries with known cases of BSE. U.S. MBM prices continued a decline that began at the end of the drought in 1988 and reached a nominal low in spring 1995 with a per ton amount that ranged from the upper $150s to the lower $160s. While there is no evidence that regulations seriously affected domestic MBM markets, the early part of the decline in U.S. MBM prices may have been induced in part by BSE-related market activity.

The 1996 announcement of a potential link between vCJD in humans and BSE in cattle elevated BSE-related concerns and shifted them from an animal health issue to a human health issue. This shift also resulted in significant feed regulations being imposed, particularly aimed at MBM. In August 1997, the U.S. Food and Drug Administration (FDA) implemented a regulation prohibiting the use of mammalian protein, primarily MBM, in the manufacture of ruminant feeds (USHHS, FDA, 1997a and b). These mammalian protein sources were excluded from feed because the suspected infective abnormal prions are thought to be transmitted in MBM rendered from infected cattle. Prior to the August 1997 ban, MBM could be used in place of or along with soybean meal, cottonseed meal, and other proteins as a source of protein in ruminant rations.

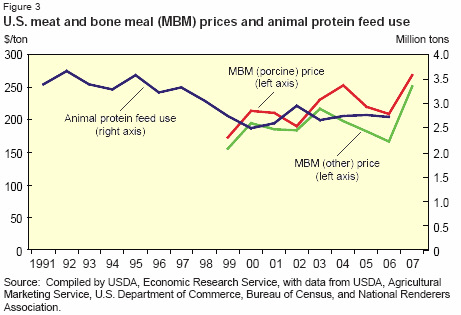

U.S. MBM prices declined by half over the next 2 years, from a high of $431 per ton in April 1997, attained in part due to drought conditions in 1996 that drove grain prices to record highs, to a low of $187 per ton in March 1999. Another significant development during this period was segmentation of the MBM market into two markets beginning in summer 1997, porcine- (derived primarily from hogs, horses, and other nonruminant animals) and ruminant-derived MBM (fig. 3). Porcine MBM averaged a premium of $15.78 per ton over the period January 1998-December 2003 (Coffey et al., 2005), just before discovery of the first U.S. case of BSE.

In assessing the economic effects of the 1997 ban of MBM in ruminant feed, FDA estimated that U.S. MBM prices would decline by between $25 and $100 per ton (USHHS, FDA, 1997a) and accepted Sparks Companies, Inc.’s estimate of a decline of $68.27 per ton (USHHS, FDA, 1997b, p. 30970). FDA rejected the assumption that other protein feeds, like soybean meal, would substitute for all MBM used in ruminant feeding, and instead assumed that only 10-15 percent would be replaced, at an estimated cost of $8 million (USHHS, FDA, 1997b, pp. 30971-30972). Annualized private-sector costs of measures implemented due to the 1997 feed ban regulations were estimated at between $21.4 million and $48.2 million (USHHS, FDA, 1997a). These estimates pertained almost exclusively to the rendering industry and markets for byproducts and rendered products. Revised FDA estimates indicated that the ban would ultimately cost the U.S. private sector approximately $53 million per year, reflecting $44 million in direct compliance costs to beef, rendering, and byproduct industry sectors (including annualized capital and operating costs), $171 million in lost value of products to the rendering industry (primarily a decline in value of MBM), and a gain of $163 million, through lower feed costs, to producers of nonruminant animals (USHHS, FDA, 1997b).

In December 2000, the United States banned imports of all rendered products from Europe for feeding, regardless of species of origin (Coffey et al., 2005). The United States also increased its surveillance by increasing BSE sampling and broadening sampling procedures to account for any regional differences in BSE incidence. These measures were characterized by increasing MBM prices and, in 2002, the narrowest price spread between porcine and ruminant MBM since reporting of the two price series began. MBM prices had recovered somewhat by 2003, with prices reaching a high of $395 in November 2003 (see fig. 1).

The United States announced a series of new regulations shortly after the December 2003 BSE discovery. These additional regulations were designed to enhance protections against the spread of BSE and to reassure consumers that beef was safe to eat. Enhanced testing objectives were also implemented in the United States to determine the extent to which BSE was present in the U.S. cattle population.

In late December 2003 and January 2004, both the FDA, the agency in charge of animal feed contents, and USDA’s Food Safety and Inspection Service (FSIS), the agency responsible for animal welfare and slaughter, imposed additional regulations to prevent the spread of BSE to humans and animals (USDA, FSIS, 2004a). These interim proposed rules, four from each agency, were followed by an FDA rule announced in October 2005 that proposed to prohibit the use of certain cattle origin materials in the food or feed of all animals (USHHS, FDA, 2005b).

In January 2004, MBM prices dropped to $173 in response to the U.S. BSE confirmation. But by April 2004, MBM prices had recovered to a peak of $397 per ton. The regulations FDA posted during summer 2004 sent MBM prices into another decline, reaching a low of $187 per ton in October 2004, a level not seen since.

Other Economic Effects

A number of feeds serve as sources for protein in livestock rations. In addition to oilseed and animal proteins, alfalfa hay and other alfalfa products are sources of high-quality protein, especially for ruminants. Wet and dried distillers’ grains also can be used as protein feeds, again, especially for ruminants. Higher prices for protein feeds would result in some limited substitution of feed grains for some protein, especially for hogs and poultry, and alfalfa for some protein, especially for cows. However, substitution of corn for protein could be limited by the use of corn to produce ethanol, which provides support for feed grain prices.

Another factor in the corn-protein substitution scenario is that a bushel of corn (56 pounds) yields about 2.7 to 2.8 gallons of ethanol and only 17.4 pounds of distillers’ grains. Thus, in terms of total feed usage, ethanol production reduces the supply of energy feeds by two-thirds (the 56:17.4 conversion). Supplies and use of wet and dried distillers’ grains, byproducts of ethanol production, are rapidly increasing as ethanol production increases. The increased use of these increased supplies of distillers’ grains would likely have offsetting effects on any increases in the prices of other protein feeds stemming from regulatory restrictions on MBM use. Because the nutrient profile of distillers’ grains exhibits high levels of both protein and energy, the increasing use of distiller’s grains at attractive prices is a confounding factor in any BSE-related, and, therefore, protein-related analysis.

The regulatory measures announced by both FDA and FSIS in late December 2003 and January 2004 required slaughterhouses to remove additional products from cattle and implicitly challenged industries to find new uses for or means to dispose of materials on the expanded list of cattle materials prohibited from animal feeds (CMPAFs, formerly SRMs, or specified risk materials) and other materials banned from human or animal consumption. As a result, production costs increased and revenues declined for producers and processors of beef products and byproducts.

If future regulatory activities were to implement enhancements originally proposed by FSIS and FDA in 2005 or further enhancements, other protein meal markets could be significantly affected. For example, based on earlier analyses, if the extreme version of the MBM ban were adopted (no mammalian protein fed to any animals), estimates of price increases for other protein sources range as high as 100 percent (Coffey et al., 2005). Many view such an increase as unlikely, given the current MBM share of total protein feeds and sources, which most recently, includes increasing quantities of distillers’ grains. Preliminary research at ERS (Mathews and McConnell, 2008) suggests more modest price changes for other proteins for the 13.6-percent supply shock assumed by Coffey et al. (2005).

In addition, Coffey et al.’s 13.6-percent decrease in protein meal supplies was based on MBM shares of total proteins prior to the 1997 feed ban. More recently, MBM represents a less-than-8-percent share of total proteins (excluding proteins in such feedstuffs as alfalfa hay, distillers’ grains, and corn gluten feed). Given a less-than-8-percent share, a complete ban would likely result in a much smaller increase in soybean meal and other protein prices than Coffey et al.’s estimate of 100 percent.

| Table 1 Economic effects of BSE-related feed regulations banning meat and bone meal proposed by the U.S. Food and Drug Administration on selected livestock-related sectors | ||

| Affected sector | Per unit effects | Estimated aggregate annual effects |

|---|---|---|

| Dollars | Million Dollars | |

| Increase in meat and bone meal pricesa | 25-100/ton | 8 |

| Increase in definition of specified risk materialb | 2.16-6.77/head | 195 |

| Increase in costs of feeding cattleb | 23.61/head | 637 |

| Net of loss to rendering and gain to nonruminant livestock feedinga | 53 | |

| Export lossesb | 3,200-4,700 | |

| Source: Compiled by USDA’s Economic Research Service from aUSHHS, FDA (1997b) and bCoffey et al. (2005). | ||

Coffey et al. estimated that per animal costs of feeding a beef steer would increase from $18.51 (includes $4.50 for increased feed costs from substitution effects for a ruminant protein to any farmed animal) to $23.61 (includes $9.60 for increased feed costs from substitution effects for a ban against feeding any animal protein to any farmed animal) (table 1). To the extent that these estimates are based on the inflated impact of MBM on soybean meal prices and an extreme scenario, estimates of the impact of FDA’s (2008) Final Rule on steer feeding costs are expected to be much lower.

Until FDA published its 2008 Final Rule, proteins manufactured from ruminants and other animals could be fed to hogs and poultry because neither species is known to be affected by any known TSE. Because current and additional, but related, interim rules imposed by FSIS and FDA would change current feed manufacturing practices in significant ways (USDA, FSIS, 2004a and b; USHHS, FDA, 2005a and b; USHHS, FDA, 2008), the FDA Final Rule went through an extended comment and analysis period. In the meantime, the potential economic effects of these regulatory actions on the feed manufacturing industries were estimated, including those by FDA (USHHS, FDA, 2005b, 2008), Coffey et al. (2005), and Informa Economics (2005).

However, analyses for the most extreme scenario became moot with the publication of FDA’s Final Rule on April 25, 2008, a modified version of the October 2005 proposed rule (see footnote 1), which bans feeding cattle materials prohibited in animal feeds (CMPAF) in feeds for all animals. When this Final Rule is implemented in 2009, feed substitution impacts will likely be relatively small in the aggregate (Mathews and McConnell, 2008).

However, in addition to increased feed costs and other downstream costs, increased restrictions on feed ingredients have introduced an additional round of disposal issues and costs. For example, as FDA noted, renderers, who once picked up dead animals for free, become less inclined to pick up animals that cannot be rendered or will pick them up only at costs estimated at $100 or more per head (USHHS, FDA, 2008; Sparks, 2002). Disposal of additional SRMs/CMPAFs becomes an issue for packers, renderers, incinerators, and landfills in terms of increased costs and environmental concerns. Additional disposal costs for a 1,000-pound animal from which SRMs/CMPAFs can no longer be removed are estimated at $18.75 per head (Coffey et al., 2005). Estimates of increased costs of expanded SRM/CMPAF regulations, which include costs of disposing of SRMs/CMPAFs, range from $2.16 per head (cattle under 30 months old) to $6.77 per head for older animals (see table 1).

Conclusions

Meatpackers and renderers are among the first downstream users of cattle and beef products and byproducts affected during a major animal disease outbreak as regulations prohibit the entry of the meat of diseased animals into the food system. This results in supplies of raw materials (animals or meat) that cannot be disposed of through normal marketing channels. Policies and regulations implemented in the aftermath of a disease outbreak are often extensive, affect related industries, and have economic effects that last much longer than those of the disease outbreak.

While a number of costs associated with regulatory responses have been estimated, particularly for the rendering and other cattle and beef industry sectors, benefits of regulation have been neglected in this research. The most obvious benefit is reduction of risk from animal disease—in this case, risk to animals from BSE and risk to humans of vCJD. However, the incremental value of this risk reduction has not been estimated. Few would argue that reducing the risks from either the spread of BSE among U.S. cattle or to humans in the form of vCJD is not worth pursuing. However, some in the industry and other analysts have begun to ask about the tradeoffs between marginal reductions in these risks and the costs incurred in achieving these risk reductions. While benefits from risk reduction, trade gains, some gains to producers not directly affected by disease losses, and some consumer gains have been estimated, others have yet to be appropriately identified, much less valued.