US beef sector braces for another year of tight supplies - CoBank

Herd at decades-low as slaughter falls 7.9% year-to-date

10 April 2026

10 April 2026

1 minute read

1 minute read

By:

By: After a tumultuous 2025, this year is expected to come with similar volatility levels and concerns over whether the US beef sector is prepared to fundamentally fulfil consumer demand, according to a recent CoBank report. Producers faced numerous challenges last year including New World Screwworm shutting down live cattle imports from Mexico, announcements of beef processing closures or downsizing shifts due to limited cattle supplies, and increased reliance on imports, just to name a few. On top of these measures, cattle prices in every production stage hit record highs, with profitability heavily in favor of cow-calf ranchers and feedlots, and record losses for beef packers.

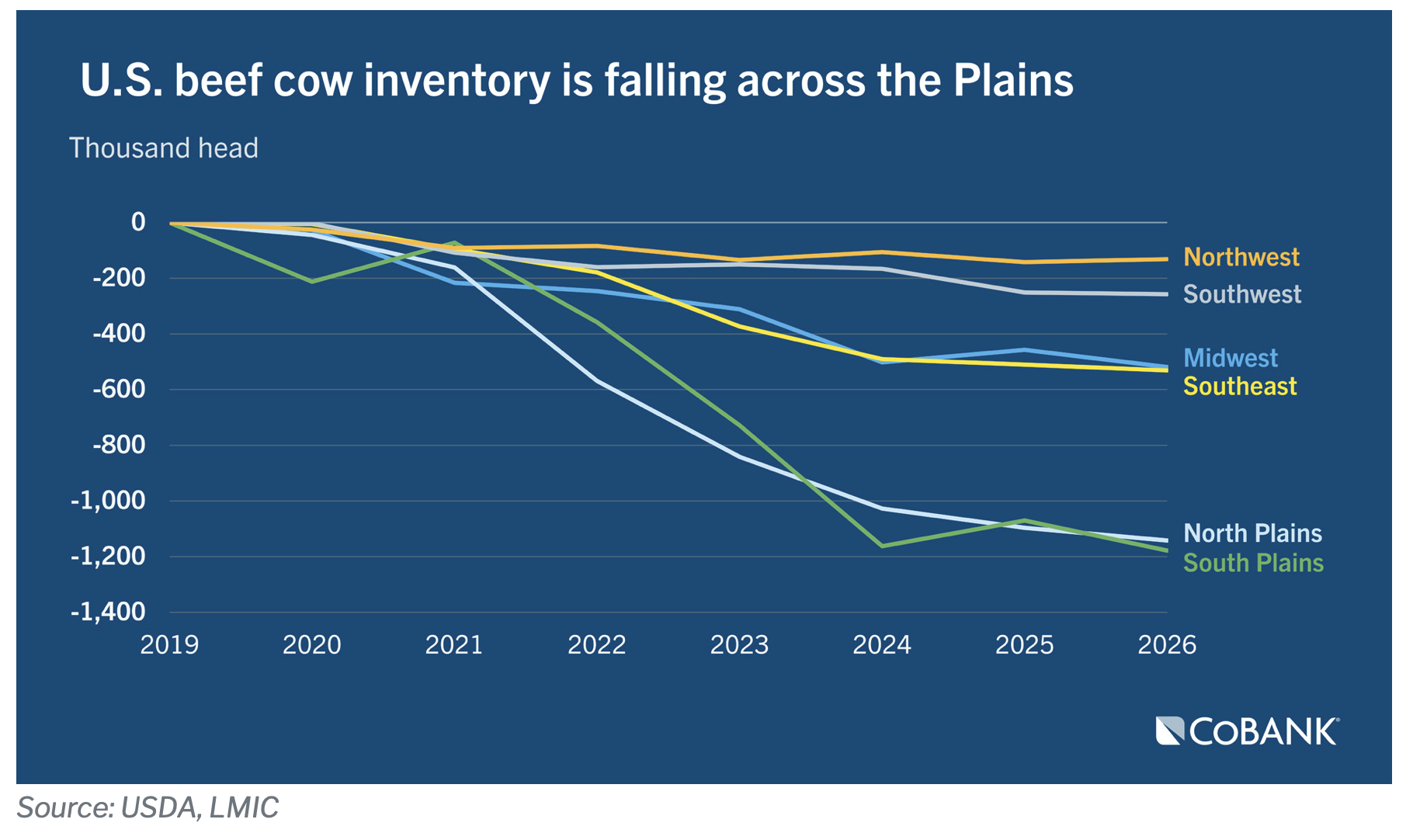

What this boils down to is restricted cattle supplies trying to deliver enough to meet demand and asking where the next generations of cattle will be raised. Beef cow inventory peaked most recently in 2019. Since then, the total beef cow herd has declined by nearly 3.8 million head. But the contraction has been more robust in the Northern and Southern Plains than any other region in the US. Essentially, this is the middle-third of the country.

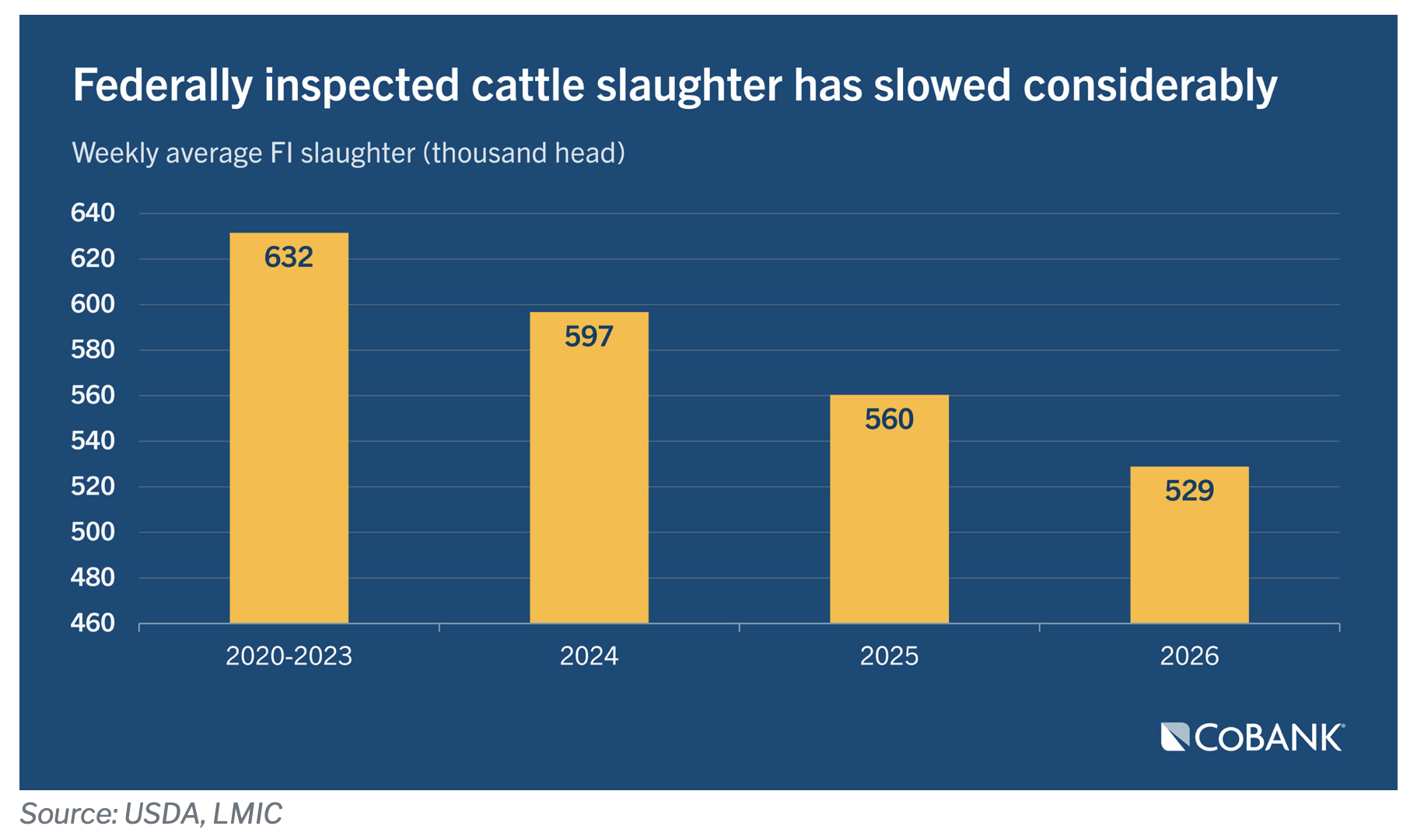

Poor pasture conditions and weak forage conditions have been the main drivers, limiting cattle availability, which is compounding the role that decreased feeder cattle imports from Mexico is adding to the market, ultimately increasing the competition for cattle in feedlots and for packers. Even more so, federally inspected slaughter has slowed considerably in 2026 due to supply limitations and winter storms in the first quarter. Federally inspected slaughter is down 547,000 head or 7.9% year-to-date.

The squeeze of record high feeder and lagging fed cattle values is beginning to drag on cattle feeders’ margins. According to Iowa State’s yearling-to-finish crush margin calculations, cattle entering feedlots in December and sold in May will net $350 per head, whereas those entering in March and sold in August are projected to lose $200 per head. Even when the herd starts rebuilding, higher prices for cattle are still expected as fewer animals will enter feedlots until cattle supplies balance out. In the meantime, utilising risk management and hedging to lock in revenue and protect against falling prices is critical during this era where the end of the bull run is unknown.