LMC:Slaughter Update Shows Tight Supplies and Competition

NORTHERN IRELAND - Reports from the plants over the last few months have indicated a tightening in the availability of prime cattle when compared to previous years, say market analysts at the Livestock and Meat Commission. 10 April 2013

10 April 2013

4 minute read

4 minute read

This has resulted in an increase in competition between the plants, particularly for good quality in-spec prime cattle.

As highlighted in previous editions of the LMC Bulletin, producers with good quality cattle that meet current market specifications are in a strong position to negotiate with the processors to achieve higher prices that initial quotes would suggest.

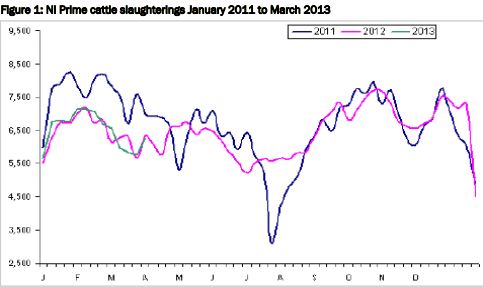

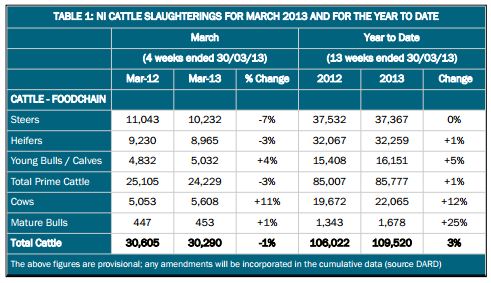

The latest slaughter statistics from DARD have indicated that the NI prime cattle kill for the first quarter of 2013 was one per cent higher than the corresponding period in 2012 at 85,777 head as indicated in Table 1. If the breakdown of the prime kill is considered between the two periods the young bull kill was up five per cent in 2013 with steer and heifer throughput relatively unchanged.

A tightening in cattle availability in the rest of GB has meant prime cattle throughput in the first

quarter of 2013 is running 4.9 per cent behind the corresponding period last year.

Meanwhile in ROI the availability of prime cattle has improved, primarily due to a reduction in calf and weanling exports in 2011 and 2012 and these animals are now coming forward for slaughter.

As a result prime cattle throughput has increased from 255,678 head in the first quarter of 2012 to 276,203 in the first quarter of 2013, an increase of eight per cent year on year.

Meanwhile the cow kill in NI increased from 19,672 head in the first quarter of 2012 to 22,065 head in the first quarter of 2013, an increase of twelve per cent between the two periods.

This increase in the cow kill has resulted in total cattle slaughterings for the year to date running three per cent ahead of this time last year, increasing from 106,022 head in the first quarter of 2012 to 109,520 head in the first quarter of this year.

However if we consider the kill for the four weeks ending the 30 March 2013 compared to the corresponding period in 2012 there has been a tightening in supply. It is also worth noting that quarter one of 2012 was a very low point in terms of production over the last five years.

The steer kill in NI during March 2013 was 10,232 head, a seven per cent reduction on the 11,043 head slaughtered in the same period in 2012.

The heifer kill in March 2013 totalled 8,965 head, three per cent lower than the 9,230 heifers slaughtered during March 2012. Meanwhile the young bull kill increased from 4,832 head to 5,032 head when comparing March 2012 and March 2013, an increase of four per cent year on year.

The combination of these has resulted in the total prime kill being back three per cent when comparing March 2012 and March 2013. The total NI cow kill in March 2013 was 5,608 head, an eleven per cent increase on March 2012 when 5,053 head were slaughtered.

However despite the combination of this strong increase in the cow kill and the four per cent increase in the young bull kill the total kill was down one per cent year on year.

Some of this decline in total slaughterings can be attributed to a reduction in the number of cattle being imported into NI for direct slaughter. In the first quarter of 2013 5,675 head of cattle were imported from ROI, an 18 per cent reduction on the 6,952 imported during the first quarter of 2012.

There has also been an increase in exports from NI to GB and ROI for direct slaughter, increasing from 4,012 in the first quarter of 2012 to 7,181 in the first quarter of 2013, an increase of 79 per cent year on year.

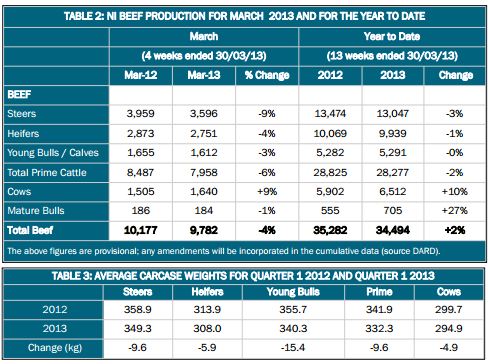

The one per cent reduction in the total NI kill combined with a reduction in average carcase weights has resulted in total beef production in March 2013 to be four per cent lower than in March 2012 as outlined in Table 2. For the year to date however there has been a two per cent increase in beef production when compared to 2012.

There was a reduction in average carcase weights recorded for all classes of cattle when comparing the first quarter of 2013 with the corresponding period in 2012 as outlined in Table 3.

Average steer carcase weights were back by 9.6kg to 349.3kg in 2013 with the average heifer housed at lower than usual liveweights in the autumn.

It is likely that this has translated into animals finishing at lower carcase weights. The reduced quality and availability of silage during this winter/spring, combined with the high cost of concentrates, may also have encouraged producers to slaughter cattle at lower carcase weights than they usually would and thus the drop in average carcase weights.

The average young bull carcase weight showed the most notable decrease when comparing the first quarter of 2012 and the first quarter of 2013, declining by 15.4kg to 340.3kg. One possible reason for this decline is that the current high cost of intensive finishing may have encouraged producers to finsh bulls at lower carcase weights.

A tightening of processor penalties for young bulls that are over 16 months of age may also have encouraged producers to finish bulls at a younger age and thus at lower carcase weights than previous years.

TheCattleSite News Desk